We often get asked, “Why PayPal?” A valid retort to an investment that has moved nowhere in 4 years. In this article, we provide our thesis behind rating PayPal as a BUY and including it in the Plebdex for several years in a row.

Investment Rating: CONVICTION BUY

12-Month Price Target: $135.00 (+100% Upside)

Long-Term Target (2030): $310.00

Current Price: ~$58.50

Implied P/E (2026E): ~10x

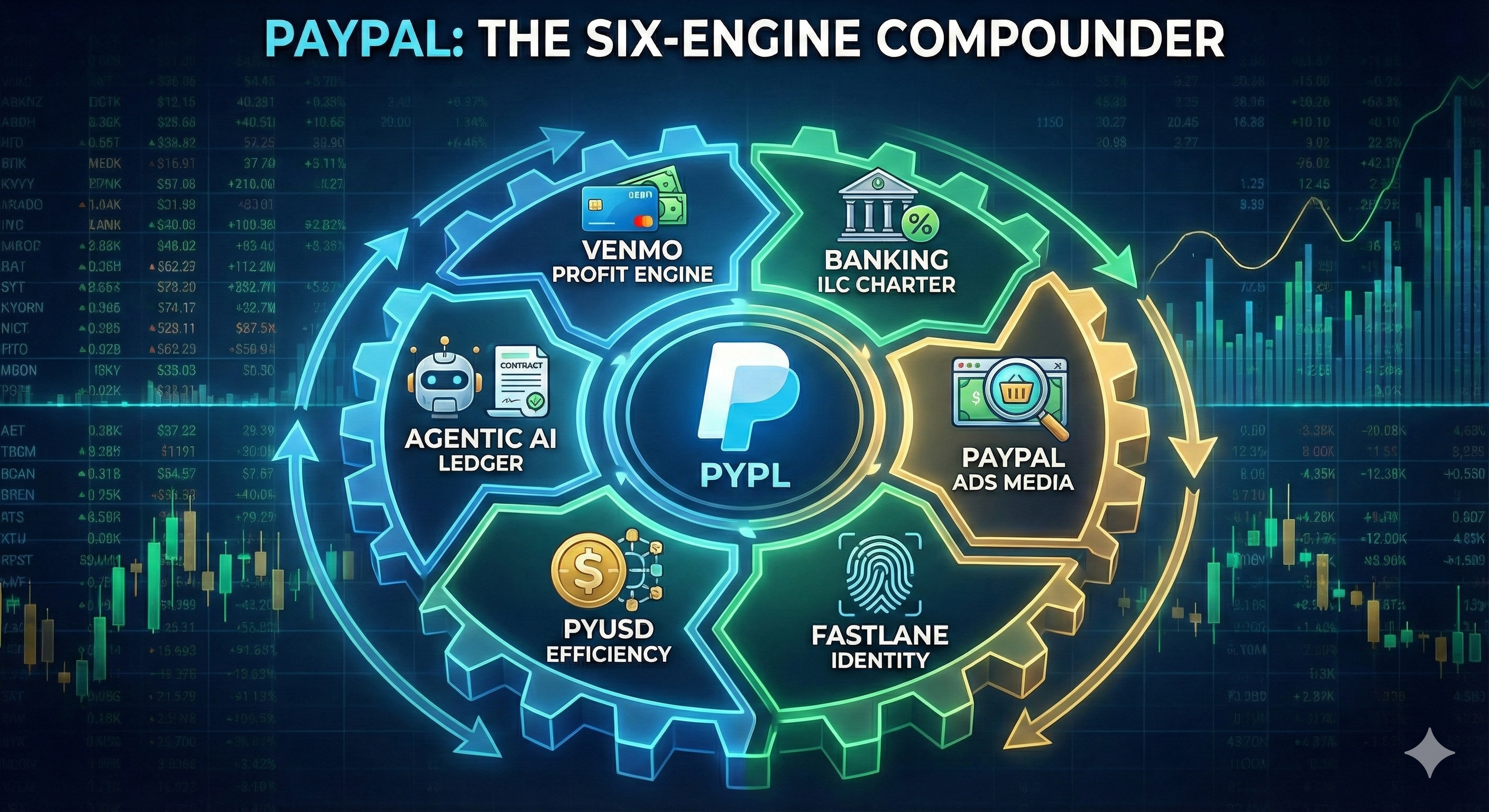

1. Executive Summary: The Asymmetric Dislocation

The consensus view on PayPal—that it is a legacy “checkout button” fighting a losing war of attrition against Apple Pay—is structurally flawed. It ignores the fundamental pivot that solidified in late 2025: PayPal has evolved from a commoditized payment processor into a Closed-Loop Commerce Ecosystem.

We are witnessing a rare dislocation where a high-quality compounder is priced like a dying asset. Our “Conviction Buy” thesis is not predicated on hope for user growth, but on six synchronized margin engines that are actively re-pricing the business.

Unlike previous years, where growth was driven by low-margin volume, 2026 marks the beginning of a “Margin Super-Cycle” driven by Banking Verticalization, Media Monetization, and Identity Resolution. At 10x forward earnings, investors are paying for zero growth but receiving a business capable of compounding EPS at 20%+ CAGR through 2030.

2. The Profit Engine: Venmo’s Commercial Inflection

The “Free User” era is over. Venmo has graduated from a viral utility to a consumer neobank.

Venmo has long been a drag on margins. That narrative is now obsolete. The “monetization gap” is closing rapidly due to a structural mix-shift.

- The Mix-Shift: In 2H 2025, “Pay with Venmo” (Commercial) volume grew +50% YoY, while P2P volume (Zero Yield) flattened. Every dollar that moves from P2P to Commercial shifts from a 0% take rate to a ~2.9% take rate.

- The “Physical” Bridge: Venmo Debit Card issuance grew +40% YoY. This is the highest-margin activity in the ecosystem (Interchange Fees) and increases user retention by ~3x compared to app-only users.

- Teen Accounts: The “Venmo Teen Account” is the ultimate lock-in mechanism, capturing the next generation of earners before they open a traditional bank account.

3. The Margin Engine: The ILC Bank Charter

Status: Filed Dec 15, 2025 | Impact: Structural Margin Expansion

This is the most underappreciated lever in the thesis. The pending Utah Industrial Loan Company (ILC) charter allows PayPal to verticalize its lending stack, eliminating the “middleman tax” paid to partner banks.

The “Cost of Funds” Arbitrage

Currently, PayPal funds its $30B+ SMB loan book via wholesale debt. The charter allows them to fund it via customer deposits.

| Funding Source | Interest Cost | Annual Cost on $30B Book |

| Current (Wholesale) | ~5.5% | ~$1.65 Billion |

| Future (Deposits) | ~0.5% | ~$0.15 Billion |

| Net Savings (Pre-Tax) | ~$1.5 Billion |

Note: After accounting for operational costs and regulatory capital requirements, we conservatively estimate a $450M – $500M net lift to Operating Income annually.

4. The Growth Engine: PayPal Ads

Status: Launching Q1 2026 | Impact: High-Margin Revenue

Under the leadership of Mark Grether (formerly Amazon/Uber Ads), PayPal is launching a Retail Media Network (RMN) that monetizes its most valuable asset: deterministic transaction data [1].

- The Data Moat: Google knows what you search for. Meta knows what you click. PayPal knows what you buy. This “Closed-Loop Attribution” is the holy grail for advertisers [2].

- The Model: By opening this inventory to millions of SMBs via the PayPal Ads Manager (launched Oct 2025), PayPal is building a business with ~75% gross margins [1].

- Forecast: We project Ads to contribute $1.5B in Revenue by 2028. Because this revenue carries 3x the margin of the core payments business, it is highly accretive to the blended multiple.

Mark Grether on PayPal Ads Strategy: This video features Dr. Mark Grether, SVP of PayPal Ads, explaining the “Transaction Graph” strategy and the launch of the Ads Manager.

5. The Identity Engine: Fastlane

Status: Scaling | Impact: Conversion & Identity

Fastlane is not just an autofill tool; it is a Network Tokenization Layer that solves the “Guest Checkout” problem (40% of e-commerce).

- How Identity is Derived: Unlike competitors relying on fragile browser cookies, Fastlane queries PayPal’s vaulted database of 171M+ US device fingerprints. When a user enters an email, PayPal recognizes the device server-side and injects a secure “Network Token” to pre-fill data [3].

- Financial Impact: Fastlane users convert ~50% higher than standard guests, and checkout times are reduced by 32% [3]. This mix-shift drives ~120bps of transaction margin expansion.

6. The Efficiency Engine: PYUSD & Yield

Status: Integrated | Impact: Float Retention

Re-integrating the stablecoin thesis is critical because it has graduated from “experiment” to “infrastructure.”

- DeFi Liquidity: PayPal has partnered with Spark to scale PYUSD liquidity in DeFi markets to $1 Billion [4]. This allows PayPal to offer ~4% yields to users holding PYUSD, creating a sticky “high-yield savings” alternative [5].

- Cross-Border (Xoom): Xoom now utilizes PYUSD for cross-border settlement, eliminating “pre-funding” requirements in foreign accounts. This removes the “working capital trap” of holding idle Euros or Pesos [5].

7. The Call Option: Agentic AI & AP2

Status: Strategic | Impact: Long-Term

PayPal has successfully aligned with the Agent Payments Protocol (AP2)—the open standard developed with Google Cloud and OpenAI [6].

- The “Mandate” Concept: AI Agents (e.g., Gemini, OpenAI) cannot legally “sign” contracts. AP2 uses “Mandates”—cryptographically signed permissions that allow an agent to spend within strict limits.

- The Revenue Model: PayPal is the unique Validation Layer. On Oct 28, 2025, PayPal launched Agentic Commerce Services to verify these transactions, positioning itself as the “Visa” of the machine economy [6].

8. Financial Framework: The “Cannibal” Flywheel

We view the capital return program not as a static line item, but as a dynamic flywheel.

We model a Dynamic Capital Return Policy where PayPal commits 80% of Free Cash Flow (FCF) to repurchases.

The Mechanism:

- Margins Expand: ILC Charter + Ads drive Operating Margins from 18.5% → 25.0%.

- FCF Accelerates: Higher margins on growing revenue accelerate FCF growth.

- Buyback Compounding: A larger FCF pile retires shares at a faster rate, just as earnings power peaks.

2030 Estimates (Base Case):

| Metric | 2025 (Actual) | 2026 (Est) | 2028 (Est) | 2030 (Est) |

| Revenue ($B) | $34.5 | $37.8 | $48.2 | $62.0 |

| Revenue CAGR | — | 9.5% | 11.0% | 13.5% |

| Op. Margin | 18.5% | 20.5% | 24.5% | 28.0% |

| EPS (Non-GAAP) | $5.10 | $6.25 | $10.10 | $15.50 |

| Target P/E | 12x | 18x | 22x | 25x |

| Implied Price | $62 | $112 | $222 | $387 |

References

- PayPal Investor Relations. (2025, Oct 7). PayPal Unleashes the Power of Retail Media for Small Businesses. Link

- Marketecture. (2025, Dec 22). PayPal Open Commerce with Dr. Mark Grether: Retail Media & Agentic Commerce. Link

- PayPal Business. (2025). Guest Checkout for Your Business with Fastlane: Conversion Metrics. Link

- MEXC / Crypto News. (2025, Sept 25). PYUSD Liquidity: Unlocking Massive Growth Through PayPal’s Spark Partnership. Link

- PayPal Digital Wallet. (2025). PYUSD Stablecoin | US Dollar Crypto Rewards & Yields. Link

- PayPal Newsroom. (2025, Oct 28). PayPal Launches Agentic Commerce Services to Power AI-Driven Shopping. Link

Leave a Reply