Here’s a sentence that doesn’t get said enough: there is a legal account that lets your investments grow completely tax-free, and most people who qualify for it aren’t using it.

That account is a Roth IRA. If you’ve heard the term and glazed over because it sounds complicated, this guide is for you. By the end, you’ll understand exactly what a Roth IRA is, how the tax magic works, whether you qualify, and how to get started.

What Is a Roth IRA?

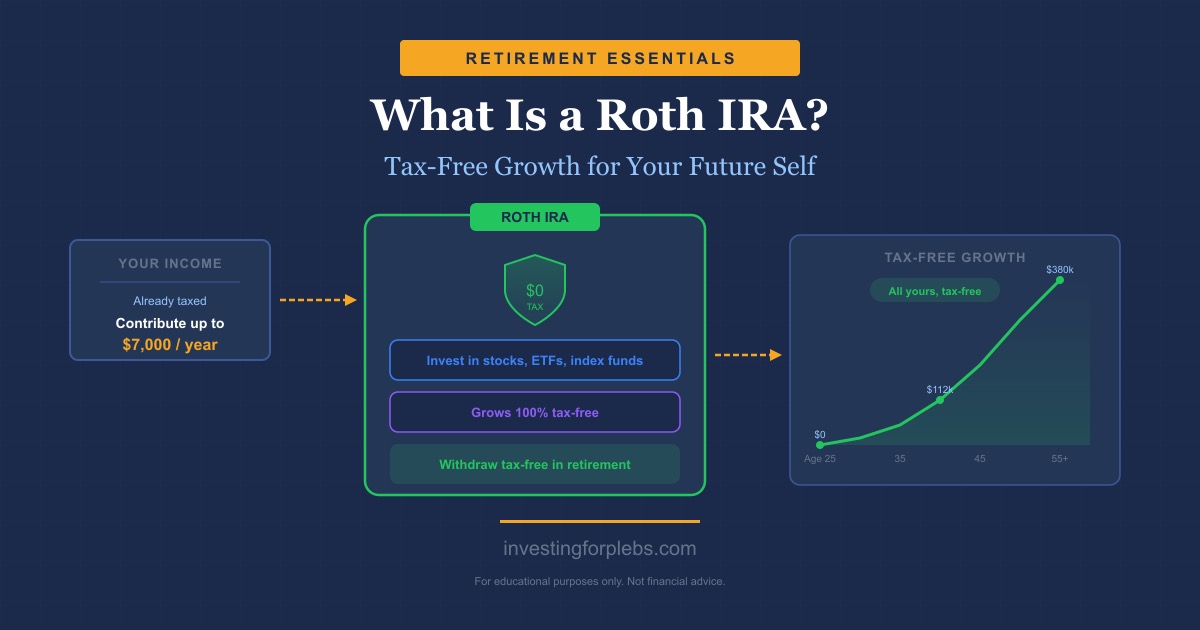

A Roth IRA is an individual retirement account that you open yourself (not through an employer). The “Roth” part comes from Senator William Roth, who championed the legislation that created it in 1997. The “IRA” stands for Individual Retirement Account.

The defining feature: you contribute money you’ve already paid taxes on, and from that point forward, the account grows completely tax-free. When you withdraw the money in retirement, you owe zero taxes on any of it, including all the growth.

That’s not a typo. Every dollar of gain, dividend, and interest that accumulates in a Roth IRA is yours to keep, tax-free, in retirement.

How a Roth IRA Works

The flow is simple:

- You earn income and pay your normal income taxes on it.

- You contribute some of that already-taxed money into your Roth IRA.

- You invest it (in stocks, ETFs, index funds, or other eligible assets).

- The money grows over time. You owe no taxes on any of that growth.

- In retirement (generally after age 59½), you withdraw the money completely tax-free.

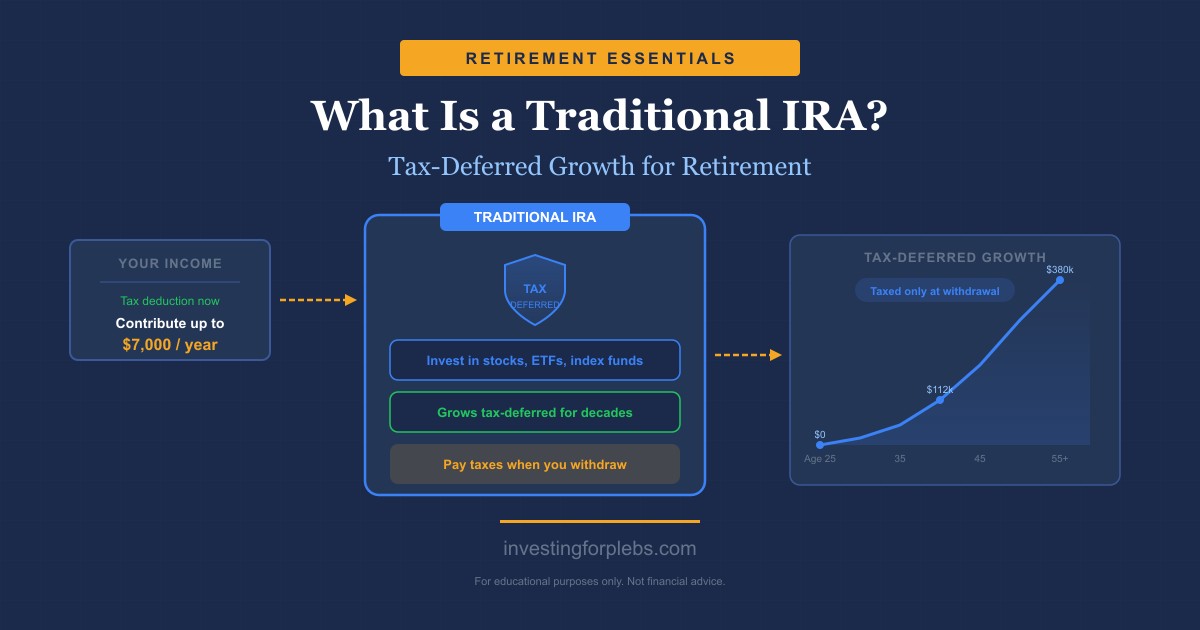

The contrast with a traditional IRA helps clarify what makes the Roth special: with a traditional IRA, your contributions may be tax-deductible now, but you pay income taxes when you withdraw the money in retirement. With a Roth, you pay taxes upfront and owe nothing later.

For young investors especially, this trade-off often favors the Roth. You’re likely in a lower tax bracket now than you’ll be later in your career. Paying taxes today on a smaller amount, then watching that money compound tax-free for decades, can produce significantly better outcomes than a deferred tax bill.

If you want to understand why compounding over time is so powerful, our compound interest explainer shows the math in plain terms.

Contribution Limits

The IRS sets annual caps on how much you can put into a Roth IRA. For 2025, the limit is $7,000 per year. If you’re age 50 or older, you can contribute an extra $1,000 as a “catch-up contribution,” bringing your total to $8,000.

A few important notes:

- These limits apply across all your IRAs combined, not per account. If you have both a Roth IRA and a traditional IRA, you can contribute a total of $7,000 between them, not $7,000 to each.

- You can only contribute up to the amount you earned from work that year. If you earned $4,000, your maximum contribution is $4,000.

- Unused contribution space doesn’t carry over. If you contribute $3,000 in 2025, you can’t add the remaining $4,000 next year on top of that year’s limit.

Note: IRS contribution limits are adjusted periodically for inflation. Always verify the current year’s limits at irs.gov.

Income Limits: Not Everyone Qualifies for the Full Contribution

Here’s the catch: the Roth IRA has income limits. If you earn too much, your ability to contribute phases out or disappears entirely.

For 2025, the phase-out ranges are:

| Filing Status | Phase-out begins | Contribution eliminated |

|---|---|---|

| Single / Head of Household | $150,000 | $165,000 |

| Married filing jointly | $236,000 | $246,000 |

| Married filing separately | $0 | $10,000 |

If your income falls within the phase-out range, you can contribute a reduced amount. Above the top threshold, you can’t contribute directly to a Roth IRA at all.

(Higher earners sometimes use a “backdoor Roth IRA” strategy — contributing to a traditional IRA and then converting it to Roth. That’s a more advanced topic beyond the scope of this guide; consult a tax professional if you’re in that range.)

Roth IRA vs. Traditional IRA

Both are individual retirement accounts. The main difference is the tax timing.

| Roth IRA | Traditional IRA | |

|---|---|---|

| Contributions | After-tax (no immediate deduction) | May be tax-deductible |

| Growth | Tax-free | Tax-deferred |

| Withdrawals in retirement | Tax-free | Taxed as ordinary income |

| Required minimum distributions | None during your lifetime | Starting at age 73 |

| Income limits to contribute | Yes | No (but deductibility phases out) |

| Early withdrawal of contributions | Can withdraw contributions penalty-free | Penalties and taxes apply |

The short version: a Roth IRA is generally better if you expect to be in a higher tax bracket in retirement than you are now. A traditional IRA may be better if you expect to be in a lower bracket in retirement and want the deduction today.

For most beginners (younger, earlier in their career, currently in a moderate tax bracket), the Roth IRA is a strong default choice.

Roth IRA vs. a Regular Savings Account

People sometimes ask: why not just save money in a regular savings account?

The difference is significant. A regular savings account has no tax advantages. Any interest it earns is taxed as ordinary income every year. When you pull money out, you’ve already paid taxes on the earnings annually.

A Roth IRA flips this entirely. Growth is never taxed again. Over 30 years, this compounding without tax drag can produce dramatically different outcomes.

That said, a Roth IRA is for retirement. You can withdraw your contributions (not earnings) at any time without penalty, but early withdrawal of the earnings generally triggers taxes and a 10% penalty. A regular savings account is more accessible for short-term goals. Use both strategically: liquid savings for near-term needs, a Roth IRA for long-term wealth.

Who Should Consider a Roth IRA

A Roth IRA is worth considering if:

- You’re early in your career and currently in a lower tax bracket

- You expect your income (and tax rate) to rise significantly over time

- You want tax-free income in retirement (fewer surprises in retirement planning)

- You don’t like the idea of required minimum distributions at age 73

- You already have a 401(k) at work and want additional tax-advantaged savings

If your employer offers a 401(k) with a match, capture that full match first before funding a Roth IRA. The employer match is an immediate 100% return on those dollars — nothing beats that. Once you’re capturing the full match, a Roth IRA is typically the next best place for retirement savings. You can read about the broader picture in The Complete Beginner’s Guide to Investing.

How to Open a Roth IRA

Opening a Roth IRA is straightforward:

- Choose a brokerage. Any major online brokerage offers Roth IRAs. Look for no account minimums, low fees, and access to low-cost index funds and ETFs. Our How to Open a Brokerage Account guide walks through the process in detail.

- Open the account. Select “Roth IRA” as your account type. You’ll need your Social Security number, basic personal information, and employment details.

- Fund the account. Link your bank account and make a contribution. You can contribute all at once or make smaller regular contributions throughout the year.

- Invest the money. This step is critical. Money sitting in a Roth IRA uninvested earns almost nothing. Choose your investments, typically low-cost index funds or ETFs. The account type doesn’t do the work; the investments inside it do.

- Set up automatic contributions. Automating monthly contributions makes this a habit rather than a decision you have to make every year.

Common Roth IRA Mistakes

Contributing without investing. Opening a Roth IRA and leaving the cash sitting uninvested is one of the most common beginner mistakes. Your money needs to be invested in something to grow.

Waiting until you “have more money.” Even small contributions benefit from years of tax-free compounding. Start with what you have, not what you wish you had.

Withdrawing earnings early. You can withdraw your contributions (the money you put in) from a Roth IRA at any time without penalty. But the earnings (growth) have different rules: withdrawing them before age 59½ and before the account has been open five years typically triggers taxes and a 10% penalty. Know the difference.

Exceeding income limits. If your income rises above the phase-out threshold and you still contribute the full amount, the IRS calls it an “excess contribution” and charges a 6% annual penalty until you fix it. Check your income eligibility each year.

Ignoring tax-loss harvesting opportunities. While the Roth IRA itself is already tax-advantaged, understanding tax-loss harvesting in your taxable accounts can complement your overall tax strategy.

The Bottom Line

The Roth IRA is one of the best financial tools available to ordinary investors. Tax-free growth over decades, no required withdrawals in retirement, and flexible access to contributions make it hard to beat for long-term wealth building.

If you’re under the income limits, have earned income, and aren’t maxing one out already, that’s worth changing. Open an account, fund it regularly, invest in low-cost diversified funds, and let time do the rest.

The tax-free version of your future self will thank you.

This content is for educational purposes only and does not constitute financial advice. investingforplebs.com is not a registered investment advisor. Please consult a qualified financial professional before making investment decisions.

Leave a Reply